Ripple vs SWIFT : the battle for the future of cross border payments

Since several years now, the boiling cryptocurrency ecosystem have seen emerge many players aiming to revolutionnize the world by bringing the internet of value across every aspects of our life. However, none of them before Ripple adopt such a bank centric approach in order to bring the internet of value not to the end users but to the bank themselves. So, as investors, it appears interesting, knowing the growth potential of the cryptocurrency area, to investigate a little bit more about this player which seems to gain traction every day and analyze whether or not the Ripple company is equipped to take over the monopole on international payments currently held by SWIFT and, as such, be a good investment for the years to come.

But first, what is Ripple ?

Ripple is an american fintech specialize on payment systems wich aims to create a new way to move money between banks and as such replace SWIFT as the banking industry network of choice. To this end, during the last 5 years or so the Ripple team developped a new answer to the five main problems of electronic fund transferring ( confidentiality, access control, integrity, data origin authentication and non repudiation) based on the blockchain technology allowing them to present a faster and more reliable manner to handle inter-bank payment.

Ripple technology vs SWIFT technology

For the most part, the SWIFT solution still relies on what we call the TT method which is nothing more than the digitalization of the 600 years old correspondant banking system and its normalization by SWIFT messages and ISO 20022 payment instructions. However, this system includes many agents and requires a lot of interactions and time in order to process a payment instruction allowing in some cases the emergence of a certain opacity around the numerous transactions and fees perceived along the process,

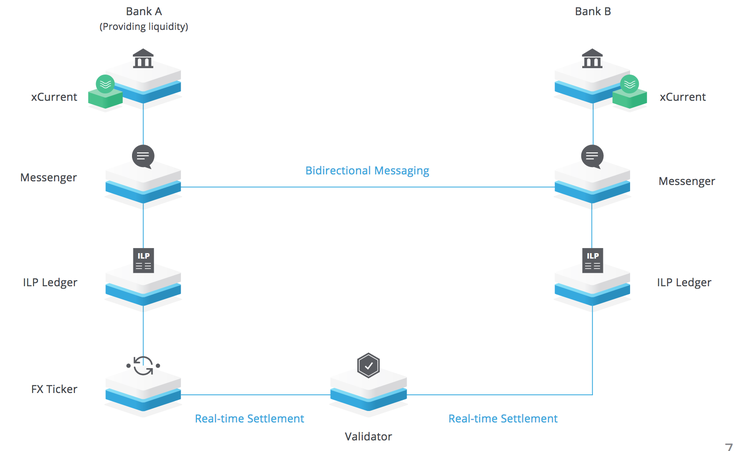

On the contrary, the Ripple solution called xCurrent redefines entirely the way of operating payment processing by using a new network called RippleNet based on the exchange of information through a network where messages are secured using a method relying on the consensual validation of encrypted hashes allowing as such the direct exchange of payments between banks.

Illustration of the key steps of the xCurrent process for international payments :

Step 1: the originating bank sends out a request for quotation across the RippleNet network for a specific payment using the API-based messaging module called messenger and obtains information relative to risk and compliance, fees, FX rates, payment details and expected time of fund delivery.

Step 2: The originating bank accepts the best quote which meets its compliance requirements and the beneficiary bank lock the quote on its side. Also it's important to note that at this point the funds are block in the two banks' ledger by the network.

Step 3: The originating bank transfers the funds out of the payer's account and trough the ILP ledger to the beneficiary bank or to the FX.

Step 4 : The beneficiary bank confirms that funds have been credited to the beneficiary's account

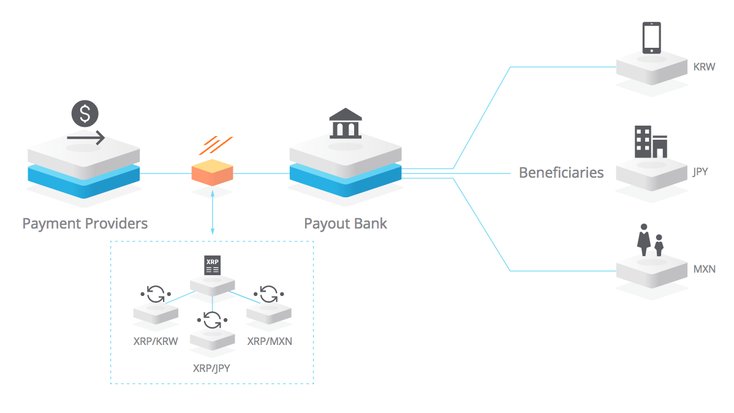

However, the xCurrent solution is not the only one proposed by the Ripple company. Indeed, they also propose the xRapid solution which through the use of the architecture created by xCurrent and the XRP cryptocurrency provides more liquidity, faster transactions and only requires banks to have a unique XRP wallet instead of having to keep numerous nostro/vostro accounts for their international payments.

So, if we strictly compare the efficiency of the SWIFT and Ripple network we can easily see that RippleNet solutions appears to be serious challengers for the TT method. Indeed, they are faster, more transparent and cheaper than the current SWIFT process.

Also, as shows the recent hack of Russian and Indian banks, the current state of the SWIFT architecture network is such that hackers only need to have access to one terminal inside the bank to be able to perform fraudulent transactions, since at the the periphery of the current payment network single signature methods are most of the time used to secure the access to the SWIFT network. In this sense, the transition to the Ripple network could be a great upgrade due to its use of multi-signing allowing banks to require customer's cryptographic signatures on transactions in order to prevent any individual bank employee to transfer customer funds on their own.

Investing in Ripple

Currently, numerous banks have partnered with Ripple and are starting to implement xCurrent like in Japan but as explained before xCurrent does not involved the XRP token in its process and Ripple is not listed on the NASDAQ. However, if we look at the bigger picture, it's easy to spot that even though banks are for now doubful about xRapid due to the volatility of the XRP token it will be the next natural step in the adoption of the RippleNet network. So, one good way to bet on the future development of Ripple in the payment industry could be to buy XRP on cryptocurrency exchanges such as Kraken or Bitstamp in order to profit from the future transition from xCurrent to xRapid.

Disclaimer : The information contained in this article relies on my personal beliefs, and the information and/or documents contained do not constitute professional investment advice.

All information/documents contained in this website rely solely on my personal beliefs, and do not constitute professional investment advice.

Be careful in your investment and do not invest more than you can afford to loose.

Contact :

e-mail: christophe.richon.pro@gmail.com